Overspending? Here’s how to budget for success

By Guest Writer | 30 October 2020 | Expert Advice, Feature

Beauty industry accounts expert & qualified nail tech, Ria-Jaine Lincoln, shares a lesson on budgeting and control to ensure you don’t overspend…

The key to budgeting and control is good cash flow and I’m revealing a guide to help you get started.

The key to budgeting and control is good cash flow and I’m revealing a guide to help you get started.

I am going to focus on the Excel template although I am a huge fan of the Float app for automated cash flow that saves lots of time and stress.

The below notes will guide you with the example spreadsheet. It does take time to get this set up but once you have the key structure in place, you just review the figures as you go. Allow at least an hour for this and have your business bank account and booking system or diary to hand.

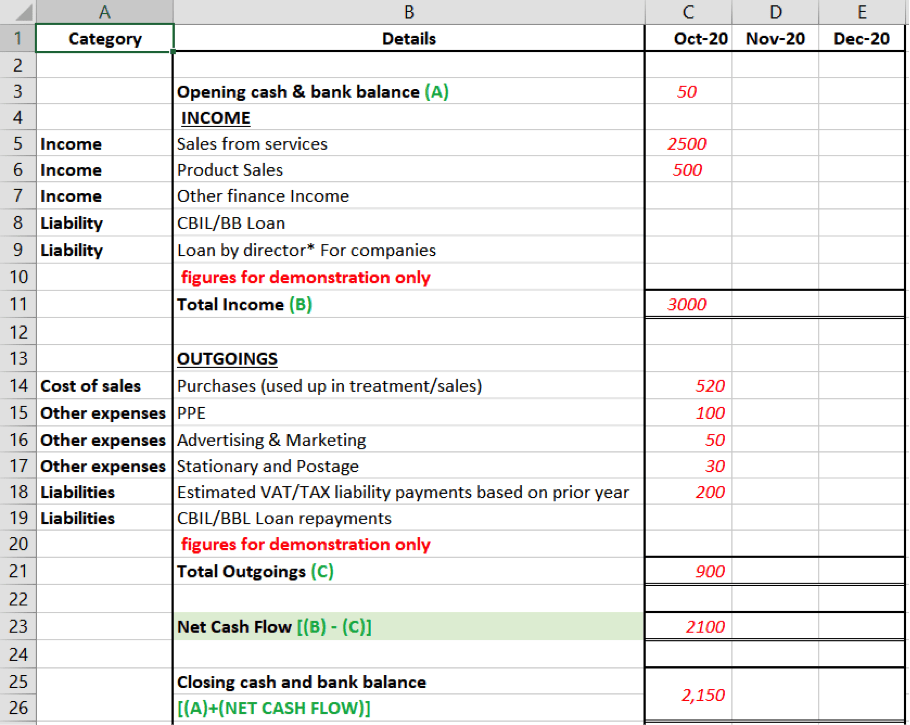

Please note: The list in Column A is not exhaustive but this should help to guide you.

Category (Column A) – The type of income or expense.

Details (Column B) – This is a short description for the income/expense. Avoid grouping income/expenses together.

Months (Column C onwards) – I find it best to work in months but you can set this up weekly.

Opening Cash Balance (Row 3) – Include the starting balance in the bank account/cash on hand. This is important to ensure your end balances are correct in row 26.

Now, start entering the Income and Expense labels and Total Headings into the spreadsheet. You will need to enter formulas in the total columns in rows 11 and 21 in the example to sum this up for you, e.g =SUM(C5:C9) for total income in October column.

Cost of Sales (row 14) – This expense is for the items that are used up when providing a service, e.g gel polish, acetone, acrylic, monomer, lint free wipes etc.

This is different to an operating/indirect expenses, so it is important to categorise this correctly both when preparing your accounts and when reviewing business performance. You can have more than one cost of sales row depending on how detailed you want the cash flow to be.

Liability – An amount that is due to be repaid by the business (row 8 and 9), so it is important to track the outstanding liabilities and plot the repayments to determine how you are going to pay this back (row 18 and 19).

Closing Cash and bank balance (Row 25/26) – When reviewing each month, this figure should match the total cash in your bank and any cash that you have on hand. If it doesn’t, you will need to double check formulas and entries made. You should review each month at the end of the month to stay on track.

Budgeting & Control – When planning future months, the closing balance shown will show what is expected to be available at the end of the month. It is best to plan at least three months and it is important to check regularly. If the closing balance is showing as negative, then you need to take action and plan how to minimise the future negative cash flow. For example, if you set up the cash flow and find -£300 in December’s closing balance, you have from now until December to cut back or push forward.

You must act as soon as you see that first negative cash flow. There are many ways that negative cash flow can be resolved but this is unique to each business.

Some examples include increasing prices, reducing costs and researching what sales should be included in your marketing campaigns to close the gap as quickly and efficiently as possible. This simple task is crucial for the survival of any business but even more so at this this time.

For more information on how to get started, how to improve negative cashflow or if you would like any help at all please do get in touch. If you don’t have the time to do this yourself it may be worth seeking the support from a professional such as myself, who can do this for you, to save time and money as a cash flow service can cost as little as a set of nails a week. This exercise can be applied to personal finances, too.

Most importantly, this is the tool to help you create a safety net which is very important to prepare for any future lockdowns or changes in circumstances – but you must act now.

Budgeting and control is one of the most important tasks for any business owner, regardless of the size or type of the business.

Friendly disclaimer: The information contained in this article is for guidance and information purposes only. It should not be relied upon as full and complete accounting, tax or legal advice. For specific advice relevant to your own situation please speak to Ria-Jaine MAAT or another professional directly.

Read the latest issue