How to keep your business finances on track

By Guest Writer | 27 May 2021 | Expert Advice, Feature

Ria-Jaine Lincoln aka The Beauty Accountant, shares top tips for keeping on top of your beauty business finances…

It has been so great to see the industry get excited and ready to re-open and now is the perfect time, at the start of the financial year and in a fresh new financial quarter, for businesses to start a review of their performance.

With April being the month the industry largely reopened, business owners should now review the business profit and loss report. This should be repeated every month or at the very least every quarter. Taking withdrawals from a business without reviewing the profit and loss position is a risky way to manage any business – no matter what size.

Additionally, reviewing the profit and loss for the first time at the end of the tax year is way too late and only useful to work out how much tax to pay to HMRC. If this sounds familiar, then you need to get started with your profit and loss review to give the business the best chance of success and the ability to grow and become profitable.

A profitable business means a regular take-home pay and profit available to re-invest back into the business for growth or innovation.

What is a profit and loss report?

The profit and loss report (P&L) is the way to interpret the business financial journey. The report takes a little time to set up in the way of organising the data if created manually but whatever method is used, it is important to use clear and relevant headings and categories for each type of expense or sale –particularly if a mix of retail, training and treatments are offered to identify the profitable areas of the business and focus points.

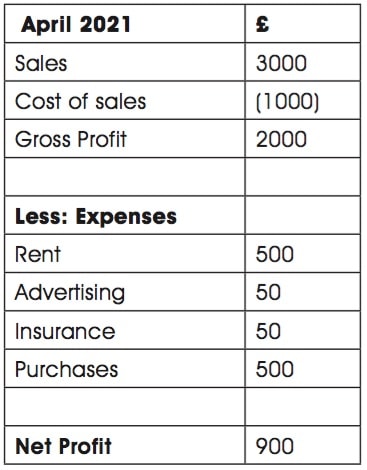

Below is a simple example of a profit and loss report:

Cost of sales (or cost of goods sold) are the direct costs involved in the sales. These are the items that are needed to produce the service or provide the goods for resale. This includes direct labour, materials (products) or shipping costs.

Expenses are the indirect costs and overheads that are due regardless of the sales that are generated, commonly referred to as the business overheads.

In service industries, it is quite common to report all the expenses under expenses as opposed to cost of sales, but this is one way to account for tax and not very useful to analyse the numbers and monitor the business performance or gross profit margins.

To produce this report, the monthly bookkeeping must be kept up-to-date, so good bookkeeping processes are important and automation is key for quick and easy profit reviews.

Different categories can be used for sales but most booking software providers will provide reports on this that can be used to review the total sales figure in the P&L. This will help business owners to work out the best performing treatments.

If already using bookkeeping software such as QuickBooks, then there is a really handy reporting section that will produce a profit and loss report for business owners at the click of a button. But remember – the report is only as good as the data within it so the bookkeeping needs to be completed correctly before running any reports. The ‘report’ option on the QuickBooks menu opens up the profit and loss option shown below. If you use Quickbooks and haven’t checked this out yet, have a look at this handy reporting feature today. Alternative software such as Xero or Freeagent will also have a reports function.

Friendly disclaimer: The information contained in this article is for guidance and information purposes only. It should not be relied upon as full and complete accounting, tax or legal advice. For specific advice relevant to your own situation please speak to Ria-Jaine MAAT or another professional directly.

Read the latest issue